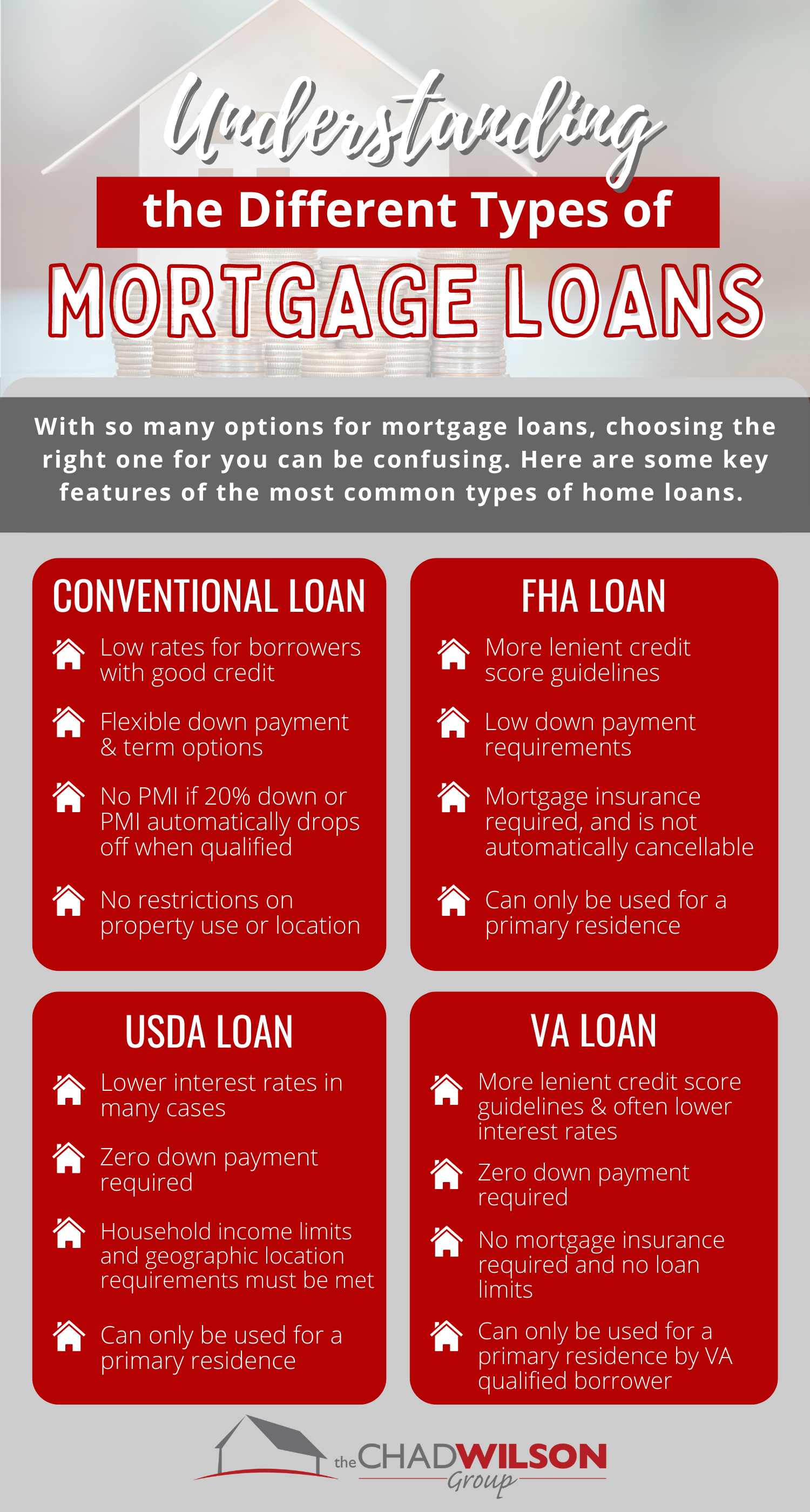

how to get a cash advance from a bank credit

What exactly is an other mortgage replacement for thought?

This information is having instructional purposes simply. JPMorgan Chase Financial Letter.An excellent. doesn’t give this type of mortgage. People recommendations discussed on this page may vary of the lender.

An other mortgage are that loan getting property owners 62 and up that have high family collateral in search of more money flow. There are numerous brand of opposite mortgage loans, but there are even selection that might operate better to suit your needs. Eg, if you find yourself handling retirement age however, wants to speak about home loan choice, specific possibilities as well as refinancing otherwise property equity financing get work most readily useful.

What is a contrary financial and just how will it really works?

A reverse home loan is actually that loan to own residents 62 and up having a large amount of household equity. The latest homeowner normally borrow funds of a loan provider from the worth of its domestic and you can have the money since the a line of borrowing from the bank otherwise monthly obligations.

When you generally consider a mortgage, first of all will come in your thoughts is an onward mortgage. An onward mortgage requires the homebuyer to spend the financial institution so you can purchase property, whereas a contrary financial occurs when the financial institution pays the fresh homeowner against the worth of their property.

Because people circulate, promote their property or perish, the opposite real estate loan is actually paid off. In the event the family depreciates within the worthy of, the fresh new resident otherwise its estate is not needed to spend the brand new differences if your mortgage exceeds the home worth.

Exactly what are the three version of opposite mortgages?

- Single-objective contrary mortgage loans: the lowest priced choice outside of the about three. He could be generally simply performed for just one objective, and this can be given of the loaner. An example would-be a giant home fix, like a ceiling replacement. Single-objective contrary mortgages are typical for property owners which have lowest so you’re able to modest income.

- Exclusive reverse mortgages: more costly and most popular getting people having increased household worth, allowing the newest debtor to view house security as a result of an exclusive lender.

- House Security Conversion process Mortgages (HECM): the most used, yet still more pricey than single-goal mortgages. HECMs was federally supported by brand new You.S. Department off Houses and you can Urban Advancement (HUD). A good HECM line of credit usually can be studied at the homeowner’s discretion, unlike the unmarried-mission contrary mortgage loans.

What is the disadvantage out-of a contrary financial

There are cons from a face-to-face home loan. When taking aside an other financial it reduces the importance of your home equity as the you might be borrowing from the bank against what you currently very own. For example, for many who very own $100K of your home therefore fool around with $50K into the an opposite mortgage, at this point you only individual $50K in your home.

An opposing financial may also affect the possession of your home down the line. If you live which have someone and take out a reverse mortgage which you or they cannot pay back, they could clean out the life preparations in case of a property foreclosure.

Bear in mind that no matter if an other home loan can present you with a credit line, youre still in charge of most other living expenses eg taxes and insurance policies.

Fundamentally, be suspicious of who you really are credit money from. There are personal enterprises if you don’t smaller genuine loan providers who you can expect to make the most of your position otherwise give you something outside of the form.

Exactly what are alternatives so you can an other home loan?

A face-to-face mortgage is generally costly and build more difficulties related to home ownership and you may obligations. There’s also the chance that you may not be eligible for an effective opposite mortgage however they are in need. Thankfully, there are many more choices available to choose https://www.paydayloanalabama.com/luverne/ from.

- Offer your house

- Re-finance

- Get a home equity loan

Promoting your home

Offering your house have a tendency to unlock your equity and give you income that can exceed the standards if for example the house worth features preferred. The fresh downside to it that you would have to move around in. Yet, if your family features appreciated in worthy of, you could sell, downsize, and you will save yourself otherwise by taking extra money.

Refinance your property

Refinancing your home could get you straight down month to month repayments and you may take back some funds. Which results in restarting this new clock towards home financing, but inaddition it form probably protecting straight down interest rates.

When you yourself have high domestic security, an earnings-aside refinance can be a good idea. An earnings-out refinance substitute your financial that have a higher financing than what you owe. The essential difference between your own original mortgage and also the financing exists into the dollars, although the loan is limited to over 80 percent of one’s household security rather than 100 %.

Domestic guarantee mortgage

Property equity financing is actually a lump sum payment of cash considering for your requirements because of the financial, using your home since security. Family guarantee fund always give competitive rates of interest and they are good to possess a-one-big date use, need repay a home improvement or any other costs.

Exactly what can reverse mortgage choices be used getting?

Reverse financial choice may come in the way of cash, a personal line of credit or a standard lump sum payment of money – based which recommendations you decide to go inside the. You can use it for home repairs or financial obligation costs, unless of course your loan standards restriction you to a specific produce.

Simple tips to pick

Looking at an other home loan or a face-to-face financial alternative depends on the age, domestic equity and what you want your loan having. If you’re 62 or more with a lot of house guarantee, an other financial would be for your requirements. Bear in mind the fresh new disappointments out of an opposing mortgage, especially the decline away from home collateral and how it might connect with the home.

An opposing home loan is a good idea during the specific issues for all those 62 or more looking to liquidate some of their home equity. There are numerous choice to that particular style of home loan which could be much better suited to both you and offer less of an aggravation in the act. Talk to a property Credit Advisor in terms of your options.